All Categories

Featured

Table of Contents

Getting rid of agent settlement on indexed annuities permits for significantly greater illustrated and actual cap prices (though still substantially lower than the cap prices for IUL plans), and no question a no-commission IUL plan would certainly push detailed and actual cap prices greater. As an aside, it is still feasible to have a contract that is really rich in representative settlement have high early cash money abandonment values.

I will concede that it goes to the very least theoretically POSSIBLE that there is an IUL policy out there provided 15 or two decades ago that has actually provided returns that transcend to WL or UL returns (extra on this below), but it's essential to much better recognize what an ideal comparison would require.

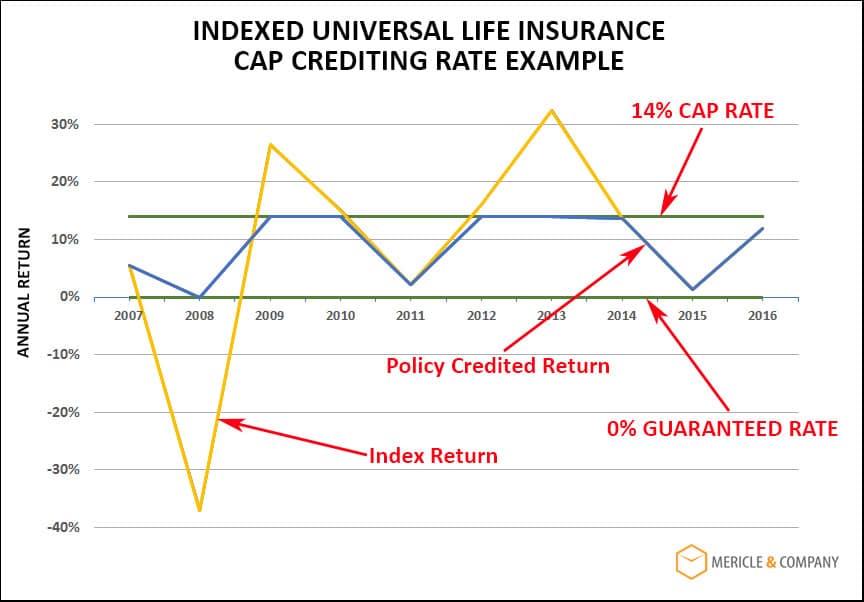

These plans usually have one bar that can be evaluated the company's discretion annually either there is a cap rate that specifies the optimum attributing rate in that particular year or there is a participation price that defines what portion of any type of favorable gain in the index will be passed along to the plan in that certain year.

And while I typically concur with that characterization based upon the technicians of the policy, where I disagree with IUL advocates is when they identify IUL as having superior returns to WL - universal guaranteed life insurance. Several IUL proponents take it an action even more and indicate "historical" information that seems to sustain their claims

Initially, there are IUL plans out there that carry more danger, and based upon risk/reward concepts, those policies ought to have greater anticipated and actual returns. (Whether they actually do is a matter for serious dispute however business are using this technique to help justify greater detailed returns.) For instance, some IUL plans "double down" on the hedging method and evaluate an additional cost on the policy every year; this fee is after that made use of to enhance the alternatives spending plan; and after that in a year when there is a positive market return, the returns are amplified.

Index Universal Life Insurance Policy

Consider this: It is possible (and in fact likely) for an IUL plan that standards a credited price of say 6% over its very first 10 years to still have a general adverse price of return during that time as a result of high costs. Many times, I locate that representatives or consumers that boast about the efficiency of their IUL policies are perplexing the attributed price of return with a return that correctly shows all of the plan charges.

Next we have Manny's inquiry. He says, "My good friend has actually been pushing me to get index life insurance policy and to join her service. It looks like an Online marketing.

Insurance coverage sales people are not negative individuals. I made use of to offer insurance at the beginning of my career. When they offer a costs, it's not unusual for the insurance coverage company to pay them 50%, 80%, even often as high as 100% of your first-year costs.

It's hard to sell because you obtained ta constantly be seeking the following sale and going to locate the next person. And especially if you do not really feel extremely convicted concerning things that you're doing. Hey, this is why this is the very best remedy for you. It's going to be difficult to locate a great deal of fulfillment in that.

Allow's speak about equity index annuities. These things are preferred whenever the marketplaces remain in a volatile period. But right here's the catch on these things. There's, first, they can regulate your habits. You'll have abandonment durations, normally seven, 10 years, perhaps even past that. If you can not obtain access to your money, I understand they'll tell you you can take a little percentage.

Iul Explained

That's how they know they can take your cash and go totally invested, and it will certainly be okay since you can not get back to your cash up until, once you're right into seven, 10 years in the future. No matter what volatility is going on, they're most likely going to be fine from a performance perspective.

There is no one-size-fits-all when it comes to life insurance policy./ wp-end-tag > In your active life, economic independence can appear like an impossible objective.

Pension, social safety and security, and whatever they would certainly taken care of to conserve. However it's not that easy today. Less employers are offering standard pension plans and lots of companies have actually decreased or stopped their retirement and your ability to count exclusively on social safety is in inquiry. Also if advantages have not been minimized by the time you retire, social protection alone was never ever meant to be adequate to spend for the way of life you want and should have.

Universal Life Quotes Online

Now, that might not be you. And it is essential to know that indexed universal life has a great deal to provide individuals in their 40s, 50s and older ages, along with people that wish to retire early. We can craft an option that fits your particular situation. [video: An illustration of a man appears and his wife and child join them.

This is replaced by an illustration of a document that reads "IUL POLICY - $400,000". The document hovers along a dotted line passing $6,000 increments as it nears an illustrated bubble labeled "age 70".] Currently, intend this 35-year-old man needs life insurance to secure his household and a method to supplement his retired life revenue. By age 90, he'll have gotten almost$900,000 in tax-free income. [video: Text boxes appear that read "$400,000 or more of protection" and "tax-free income through policy loans and withdrawals".] And needs to he pass away around this moment, he'll leave his survivors with more than$400,000 in tax-free life insurance policy advantages.< map wp-tag-video: Text boxes show up that read"$400,000 or more of defense"and "tax-free earnings via plan finances and withdrawals"./ wp-end-tag > Actually, throughout every one of the build-up and disbursement years, he'll get:$400,000 or more of security for his heirsAnd the opportunity to take tax-free income through policy fundings and withdrawals You're probably asking yourself: How is this possible? And the solution is easy. Rate of interest is tied to the efficiency of an index in the securities market, like the S&P 500. Yet the cash is not straight bought the stock exchange. Rate of interest is credited on an annual point-to-point segments. It can offer you a lot more control, adaptability, and choices for your economic future. Like lots of people today, you may have accessibility to a 401(k) or other retirement. And that's a fantastic primary step towards conserving for your future. It's important to comprehend there are limitations with qualified strategies, like 401(k)s.

And there are restrictions on constraints you can access your money without penalties. [video: Text boxes appear that read "limits on contributions", "restrictions when accessing money", and "money can be taxable".] And when you do take money out of a qualified strategy, the cash can be taxable to you as income. There's an excellent factor numerous individuals are turning to this special option to solve their financial goals. And you owe it to yourself to see exactly how this could function for your very own individual scenario. As part of an audio financial method, an indexed global life insurance policy policy can help

Indexed Universal Life Insurance For Retirement

you tackle whatever the future brings. And it supplies unique potential for you to construct significant cash value you can use as additional income when you retire. Your money can expand tax delayed through the years. And when the policy is designed effectively, circulations and the survivor benefit will not be exhausted. [video: Text box appears that reads "contact your United of Omaha Life Insurance company agent/producer today".] It is very important to talk to an expert agent/producer that understands exactly how to structure a solution such as this effectively. Before committing to indexed universal life insurance policy, below are some advantages and disadvantages to take into consideration. If you choose a great indexed universal life insurance policy strategy, you might see your cash worth expand in worth. This is useful due to the fact that you might have the ability to accessibility this money prior to the plan expires.

Given that indexed universal life insurance needs a specific level of risk, insurance business often tend to keep 6. This kind of plan additionally uses.

Usually, the insurance policy company has a vested passion in executing better than the index11. These are all variables to be considered when picking the ideal type of life insurance coverage for you.

However, given that this kind of plan is more complex and has an investment element, it can frequently come with greater premiums than various other plans like entire life or term life insurance policy. If you do not think indexed universal life insurance coverage is right for you, below are some choices to consider: Term life insurance policy is a temporary policy that generally uses protection for 10 to three decades.

Variable Universal Life Insurance Calculator

Indexed universal life insurance policy is a kind of plan that offers more control and adaptability, together with higher cash money worth development possibility. While we do not provide indexed universal life insurance, we can supply you with even more information about entire and term life insurance policy plans. We advise discovering all your choices and chatting with an Aflac agent to find the ideal suitable for you and your family.

The rest is included in the cash value of the policy after costs are subtracted. The cash money worth is attributed on a regular monthly or annual basis with rate of interest based upon boosts in an equity index. While IUL insurance policy may prove beneficial to some, it's crucial to comprehend exactly how it functions before acquiring a plan.

{kind=link}

Latest Posts

Disadvantage Insurance Life Universal

Can I Cash Out My Universal Life Insurance Policy

Index Linked Insurance